JUMP TO :

JUMP TO :

50/30/20 Budget Rule

The Simplest Salary Saving Formula for Smart Money Management

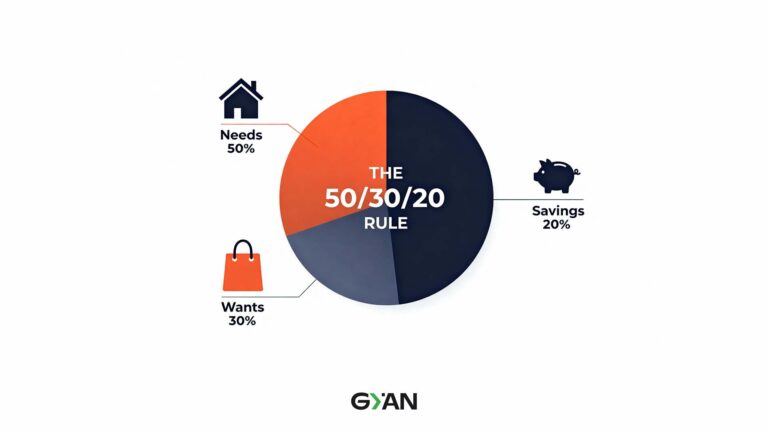

The 50/30/20 Budget Rule is an effective method to manage money and maintain a healthy financial balance: 50% needs, 30% wants, and 20% savings or debt repayment.This method allows you to keep track of how you spend your money on essential needs, on life’s pleasures and remaining on savings.

For beginners and Indian households, the 50/30/20 rule allows one to spend mindfully, save money, and balance the financial situation. It is a practical way to ensure that the expenses are controlled, reducing financial stress and creating long-term wealth without any complicated or restricted planning.

What is the 50/30/20 Rule of Budgeting?

The 50-30-20 rule of budgeting is a financial approach that allows you to manage your money without stress. This budget divides your monthly income into three categories:

-50% for needs, such as groceries, rent and bill payments

-30% for wants such as entertainment expenses, dining out etc

-20% for savings or debts payment

The purpose of the rule is to create a structure on how to spend money, live comfortably and also financially secure the future. The rule is effective in budgeting for beginners and for anyone who wishes to manage their money.

The 50-30-20 will ultimately give you a strong approach to managing your expenses until you build up and have savings while managing your money, without feeling controlled.

How the 50/30/20 Budget Rule Helps to Plan Finances?

One of the best ways to accomplish smart financial planning is through the 50/30/20 rule of budgeting. It gives psychological benefits and practical impacts and helps to know where the money is going, to reduce financial stress and become mindful in every spendings.

Psychologically, it provides clarity and ease of mind to reduce anxiety from unplanned expenses. Practically, it will make the lifestyle more sustainable and help you achieve your goals for long term financial security while also providing a foundation for better saving habits.

To maximize the use of the budgeting method, here are a few money management tips:

-Track all expenses

-Automate savings

-Revisit your budget and goals

-Establish an account (or separate) for each of the 3 categories to help eliminate overspending

Best Budgeting Tools to Simplify Financial Planning

Effective budgeting is the foundation to smart financial planning and can be simple, organized, and even fun with the right tools. As a beginner or as someone looking to tweak your money management habits, there are budgeting apps, spreadsheets, and planners out there that can help you.

For budgeting for beginners, the focus needs to be on progress and not perfection. Budgeting is about being consistent and being consistent matters more with the tools you use.

Best Tools to Try:

Budgeting Software: Budgeting tools such as Walnut, Money Manager or Goodbudget are great for tracking your expenses and organizing your spending.

- Google Sheets Templates: Free templates allow you to organize your monthly income, expenses and savings goals quickly and easily.

Personal Planner: A budgeting planner or journaling can help to stay accountable with budgeting and visualize the money journey.

How to Divide Salary Using the 50/30/20 Rule?

If you have ever wondered how to allocate your salary in a way that will benefit your future, help you cover expenses, and still allow you to live life – the 50/30/20 rule will help you accomplish that. The 50/30/20 rule is a simple model for salary budgeting in India that will also help you balance your finances and achieve your long term goals without any stress.

Step 1: Calculate Your Monthly Income

Calculate your net monthly salary amount after taxes, deductions, and EPF contributions.

For example, if your net salary amount is ₹50,000/month or ₹1,00,000/month, then that is your net salary.

Step 2: 50% Go For Needs (Essential Expenses)

Use the first half of your monthly income towards essentials such as: rent, food, EMI’s, transportation costs, and healthcare that cannot be avoided.

- For ₹50,000 salary ⇒ ₹25,000 for needs

- For ₹1,00,000 salary ⇒ ₹50,000 for needs

You will be able to maintain your same lifestyle comfortably and not worry too much about overspending.

Step 3: Set aside 30% of wants (Lifestyle Choices)

Put aside up to 30% of your expenses for non-essentials like leisure, eating out, movies, travel, subscriptions or hobbies.- ₹50,000 salary → ₹15,000 in wants

- ₹1,00,000 → ₹30,000 in wants

This way you can still have fun and enjoy your lifestyle while you are still in control of finances.Step 4: Save/invest 20% (Future plans)

The next 20% makes you invest in wealth and security using savings like: SIPs, mutual fund insurance or an emergency fund.

For example,

- ₹50,000 salary – Investing in savings/investments of ₹10,000

- ₹100,000 salary – Investing in savings/investments of ₹20,000

Following this plan makes salary budgeting in India easy and sustainable. The 50/30/20 rule provides a clear structure and ensures that every rupee earned works for present and future.

50/30/20 Rule Calculator

Applying the 50/30/20 rule makes it easy to manage your money so you can balance spending, saving, and lifestyle. With our 50-30-20 rule calculator, you can split your monthly income into ‘needs’, ‘wants’, and ‘savings’, leaving little room for error.

If you want to calculate manually, here is the saving formula!

- Needs = Income × 0.50

- Wants = Income × 0.30

- Savings = Income × 0.20

For example, if the monthly income is ₹50,000:

- Needs = ₹25,000

- Wants = ₹15,000

- Savings = ₹10,000

Make sure your daily needs are met while living your lifestyle and building savings. The 50/30/20 rule calculator makes this simple and automatic, while giving you quick results to make budgeting and financial planning easy.

It’s time to manage your money and use our 50/30/20 Rule Calculator to see how you can manage your income each month. It’s the first step to a stress-free money management experience and freedom from anxiety while saving for your long term financial freedom.

Your monthly after-tax income

Your 50/30/20 distribution:

Necessities (50%):

Wants (30%):

Savings (20%):